research

Publications and working papers in reverse chronological order.

2026

- WP

Why Is the Sovereign Greenium Small? Commitment, Pass-Through, and AdditionalityDiogo Sampaio Lima2026Working paper

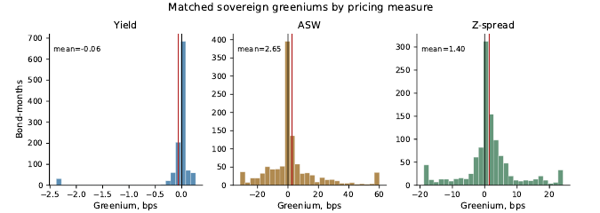

Why Is the Sovereign Greenium Small? Commitment, Pass-Through, and AdditionalityDiogo Sampaio Lima2026Working paperSovereign green bonds usually promise ordinary sovereign cash flows together with use-of-proceeds commitments. This institutional fact makes the bond-level greenium a misleading sufficient statistic for the value of the commitment. If a credible green covenant improves fiscal capacity and lowers default risk, the benefit should be capitalized into all pari-passu claims on the issuer, not only into the labelled bond. I formalize this idea by decomposing the observed greenium into an issuer-wide commitment component, a bond-specific residual wedge, and pass-through to conventional debt and CDS. The empirical evidence is consistent with this decomposition: sovereign greeniums are close to zero in yields, modest in asset-swap and z-spread measures, issuer-risk event responses are small, and official allocation reports reveal substantial heterogeneity in credibility, adaptation content, and accounting additionality. I then develop a long-term sovereign default model with climate risk, adaptation capital, and green-obligation states. In the Brazil benchmark, green access lowers mean spreads, reduces annual default risk, and raises initial-state welfare by 1.29 percent relative to regular-only borrowing, even though the model-implied bond-level commitment gain is modest. Mandatory green issuance is welfare reducing. The results imply that sovereign green bonds are best understood as state-contingent commitment options rather than as universally cheaper debt.

@unpublished{sampaiolima_greenium, title = {Why Is the Sovereign Greenium Small? Commitment, Pass-Through, and Additionality}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

NGEU Grants and Sovereign Auction Demand: Evidence from Euro-Area Primary MarketsDiogo Sampaio Lima and Martim Felgueiras2026Working paper

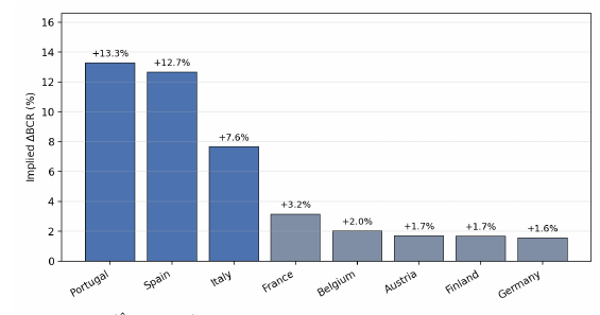

NGEU Grants and Sovereign Auction Demand: Evidence from Euro-Area Primary MarketsDiogo Sampaio Lima and Martim Felgueiras2026Working paperDoes NextGenerationEU (NGEU) raise private sovereign demand at issuance? We study this question using a 14-country panel of sovereign bond auctions from 2018 to 2023, pooling eight euro-area sovereigns exposed to NGEU grants with six non-euro-area placebo issuers. We measure auction demand using the log bid-to-cover ratio and use each country’s grants-only National Recovery and Resilience Plan (NRRP) allocation, scaled by 2019 GDP, as the source of treatment intensity after the July 2020 NGEU agreement. Because the Eurosystem is prohibited by Article 123 TFEU from buying sovereign debt at auction, the primary-market setting rules out direct ECB purchase-flow contamination, although indirect monetary-policy channels through secondary-market conditions remain possible. Auction demand rises more strongly for euro-area sovereigns with greater grants exposure: the implied bid-to-cover responses are 7.6% for Italy, 12.6% for Spain, and 13.3% for Portugal. The result is robust to inference designed for few country clusters, including exact wild cluster bootstrap and a country-label permutation test. A grants-versus-loans horse race sharpens the interpretation: the grants effect strengthens when loans are co-estimated, the loans component enters with the opposite sign, and the two coefficients are statistically distinguishable at the 1% level. The effect concentrates in the second half of 2022, consistent with a credibility interpretation in which repeated successful disbursement events built market confidence in the joint-borrowing arrangement.

@unpublished{sampaiolima_ngeu_auctions, title = {NGEU Grants and Sovereign Auction Demand: Evidence from Euro-Area Primary Markets}, author = {Sampaio Lima, Diogo and Felgueiras, Martim}, year = {2026}, note = {Working paper}, } - WP

Conditional Sovereign Backstops: Price Compression, Fiscal Eligibility, and WelfareDiogo Sampaio Lima2026Working paper

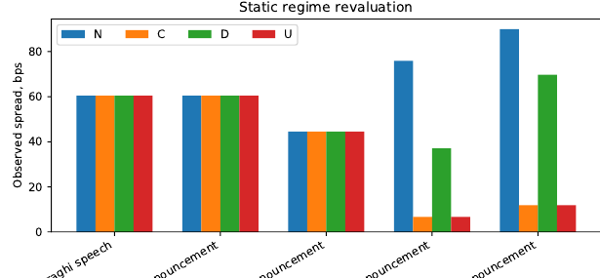

Conditional Sovereign Backstops: Price Compression, Fiscal Eligibility, and WelfareDiogo Sampaio Lima2026Working paperEuro-area sovereign backstops such as OMT and TPI promise market stabilization without an unconditional fiscal transfer. This paper studies that promise in a long-term sovereign-default model with risk-averse lenders, global risk premia, fiscal eligibility, and an eligibility-conditional support price. The key distinction is between the transaction price paid by the sovereign and the shadow private valuation of the same claim. In a Spanish calibration, committed support lowers observed spreads sharply at eligible stress states and in dynamic replay, while leaving a positive private-market risk premium. The calibration matches debt/GDP and calm spreads, delivers the right order of event-window price compression and broad official absorption, and underpredicts purchases in the narrower compliant-stress sample. Welfare does not follow mechanically from spread compression. Fixed-policy incidence accounting gives commitment a positive value relative to discretion, and a Floden-style decomposition shows that this gain is almost entirely a level effect rather than a change in lifetime uncertainty or ex-ante state risk; the benchmark value-function comparison nevertheless assigns support regimes negative transition consumption-equivalent values once borrowing incentives and intervention costs are included.

@unpublished{sampaiolima_backstops, title = {Conditional Sovereign Backstops: Price Compression, Fiscal Eligibility, and Welfare}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

Oil Supply Shocks and the Common Financial Cycle in Emerging-Market Sovereign Spreads: A Risk-Premium ChannelDiogo Sampaio Lima2026Working paper

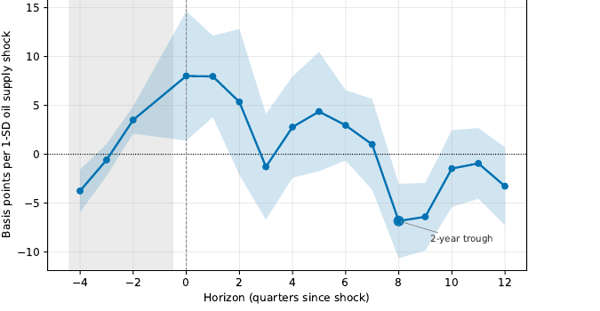

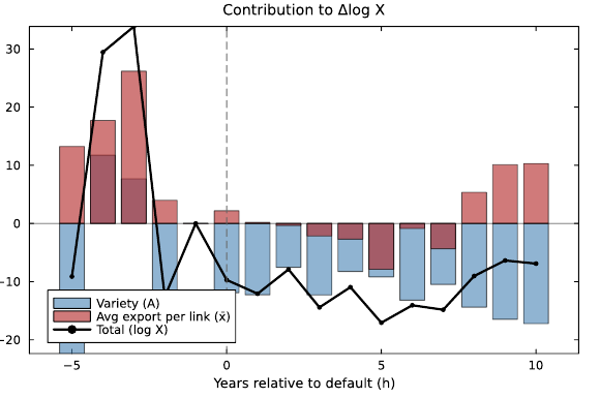

Oil Supply Shocks and the Common Financial Cycle in Emerging-Market Sovereign Spreads: A Risk-Premium ChannelDiogo Sampaio Lima2026Working paperA structurally identified positive oil-supply shock — one that lowers the oil price for reasons orthogonal to global demand — narrows the common emerging-market financial-cycle component of sovereign credit spreads at medium horizons. The sign is the opposite of the revenue-only terms-of-trade prediction of oil-exporter sovereign-default models, under which a lower oil price erodes the fiscal base and should widen spreads. Estimating lag-augmented panel local projections of five-year CDS spreads for ten oil-exporting emerging markets on the common Baumeister and Hamilton [2019] structural oil-supply shock, we find that the common-component response troughs at the two-year horizon at −3.7 basis points per one-standard-deviation shock, statistically significant under inference designed for few-cluster, single-aggregate-shock panels (wild-cluster bootstrap and Ibragimov–Müller p < 0.002). A premium-versus-loss decomposition shows that the narrowing is a risk-premium phenomenon, not a default-probability one: the physical expected-loss component built from agency ratings does not move, while the risk-neutral pricing component tracks the spread. The response is mediated through measured global financial conditions — roughly a quarter of the two-year effect runs through an intermediary-capital factor that the shock itself eases — carrying the fingerprint of the global financial cycle. The evidence implies that a quantitative model of oil-exporter sovereign risk needs a global-financial-cycle pricing block alongside the revenue/default block; without the former it predicts the wrong medium-horizon sign. We sketch such a model and use the estimated response as a calibration target.

@unpublished{sampaiolima_oil_spreads, title = {Oil Supply Shocks and the Common Financial Cycle in Emerging-Market Sovereign Spreads: A Risk-Premium Channel}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

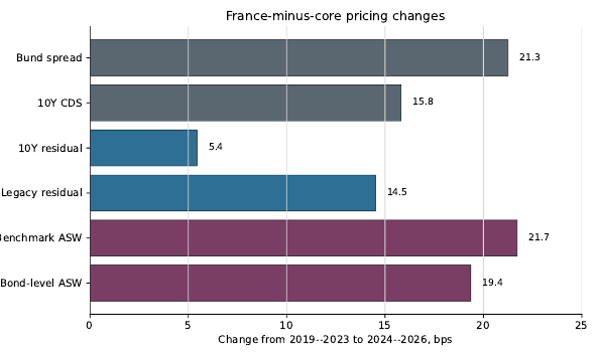

Erosion at the Core: Measuring France’s Safe-Asset Transition, 2024–2026Diogo Sampaio Lima2026Working paper

Erosion at the Core: Measuring France’s Safe-Asset Transition, 2024–2026Diogo Sampaio Lima2026Working paperCan a large core sovereign begin to lose its safe-asset standing before a default crisis makes the loss obvious? Studying France through its 2024–2026 political and fiscal turmoil, I find that markets reveal the erosion gradually and in real time, and I build a framework to detect it. Applied to this hard case—a large, liquid, core issuer with no default in sight—the framework shows French government-bond pricing pulling away from the euro core: France comes to be priced as an idiosyncratic outlier, not as a sovereign converging to the troubled periphery. The repricing is not explained by default risk, which I strip out using credit-insurance prices, nor by how cheaply the bonds trade. What remains looks like an erosion of the premium investors pay for safety itself, as the pool of close substitutes widens around France. That expanding supply contributes, though its size is not precisely identified.

@unpublished{sampaiolima_france_safe_asset, title = {Erosion at the Core: Measuring France's Safe-Asset Transition, 2024--2026}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

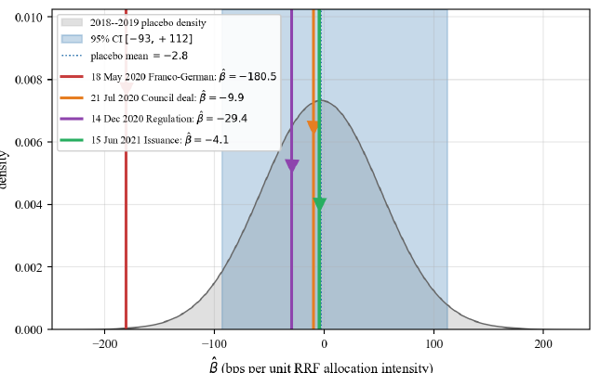

Finite-Sample Inference for Small-N Empirical Designs: Four Diagnostics from the NGEU Sovereign-Spread DebateDiogo Sampaio Lima2026Working paper

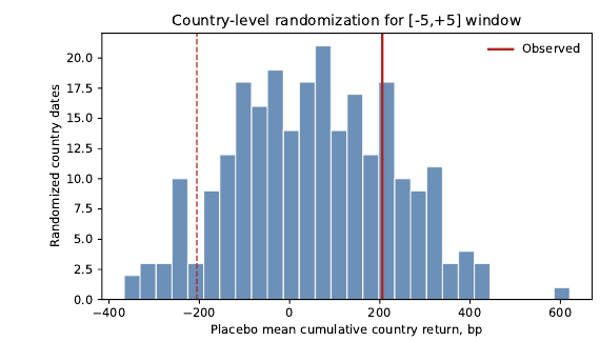

Finite-Sample Inference for Small-N Empirical Designs: Four Diagnostics from the NGEU Sovereign-Spread DebateDiogo Sampaio Lima2026Working paperThis paper studies finite-sample inference in small-N applied empirical designs, using the debate on the effects of Next Generation EU (NGEU), the European Union’s pandemic recovery programme, on euro-area sovereign spreads as a laboratory. The setting is empirically attractive but fragile: identification relies on a small number of countries, thin event-study cross-sections, continuous treatment intensity, and formula-based exposure measures. The paper shows that standard event-study inference rejects on 36–43% of clean pre-NGEU placebo trading days at a nominal 5% level, implying that conventional p-values cannot reliably distinguish NGEU news-day coefficients from ordinary pre-treatment cross-sectional spread movements in this design. The paper develops a practical diagnostic framework that links these failure modes to placebo-date calibration, few-cluster inference corrections, continuous-dose pre-trend diagnostics, and reduced-form and balance checks for formula-based exposure. Applied to NGEU, the framework substantially narrows the reduced-form evidence. Among four major NGEU news dates, only the 18 May 2020 Franco-German proposal lies outside the calibrated placebo distribution at short symmetric windows. Four-cluster auction specifications hit the wild-bootstrap p-value floor; monthly continuous-dose designs load on pre-2020 peripheral convergence; and formula-based exposure inherits the same pre-trend despite a strong first stage. The contribution is a portable decision framework and reporting standard for small-N empirical designs.

@unpublished{sampaiolima_finite_sample, title = {Finite-Sample Inference for Small-N Empirical Designs: Four Diagnostics from the NGEU Sovereign-Spread Debate}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

The Market Value of Releasable Capital: Positive-Neutral CCyB Frameworks and European Bank PricesDiogo Sampaio Lima2026Working paper

The Market Value of Releasable Capital: Positive-Neutral CCyB Frameworks and European Bank PricesDiogo Sampaio Lima2026Working paperPositive-neutral countercyclical capital buffer frameworks change the timing and interpretation of macroprudential capital requirements: banks build releasable buffers in normal times rather than only after credit booms. This paper studies how listed-bank equity markets price that regime change. A valuation framework shows that announcement returns are theoretically ambiguous because the market value of future buffer release must be weighed against the private normal-times cost of higher required capital. I construct a country-level chronology of positive-neutral and early-activation CCyB frameworks in Europe and match it to listed-bank daily equity data, MOVE, sovereign benchmark controls, historical EBA balance-sheet measures, public ECB Pillar 2 requirement data, and V-Lab stress-risk proxies. Pooled bank-level event regressions show a positive [−5,+5] response of about 32 basis points per event-window day, but the evidence weakens under country-level inference, clean-event restrictions, and a diagnostic recoding of Spain’s event date. Mechanism diagnostics using EBA variables, public buffer-distance proxies, SRISK, and LRMES do not support a simple weak-bank channel, and current local bond files contain sovereign benchmark controls rather than issuer-level bank-bond spreads. The results suggest that PNR-CCyB announcements are market-relevant, but they do not by themselves establish a clean causal effect or a settled bank-level channel.

@unpublished{sampaiolima_releasable_capital, title = {The Market Value of Releasable Capital: Positive-Neutral CCyB Frameworks and European Bank Prices}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

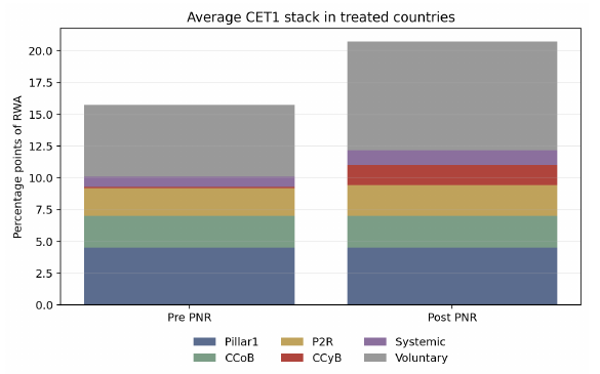

Releasable or Relabeled? Positive-Neutral CCyB and Management-Buffer Crowd-OutDiogo Sampaio Lima2026Working paper

Releasable or Relabeled? Positive-Neutral CCyB and Management-Buffer Crowd-OutDiogo Sampaio Lima2026Working paperWhen bank regulators create a releasable capital buffer in normal times, do banks add capital, or do they relabel capital they already intended to hold? I study this question using positive-neutral countercyclical capital buffer (PNR-CCyB) frameworks in Europe, where adoption is staggered across countries. I combine EEA bank-quarter capital data with country PNR adoption dates, macroprudential buffer rates, per-bank Pillar 2 requirements, and listed-bank payout data. I identify the effect by comparing treated banks to not-yet-treated controls under parallel trends in a staggered difference-in-differences design. After PNR adoption, the regulatory requirement rises by 0.97 percentage points and the voluntary buffer falls by 1.63 percentage points (1.17 to 1.63 across estimators); total CET1 does not significantly change. The composition of the CET1 stack shifts; its quantity does not. PNR-CCyB frameworks can therefore raise legal releasability without adding new capacity to bear losses.

@unpublished{sampaiolima_releasable_relabeled, title = {Releasable or Relabeled? Positive-Neutral CCyB and Management-Buffer Crowd-Out}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WP

Public Windows into Private Credit: BDC Disclosures and Same-Borrower Valuation DisciplineDiogo Sampaio Lima2026Working paper

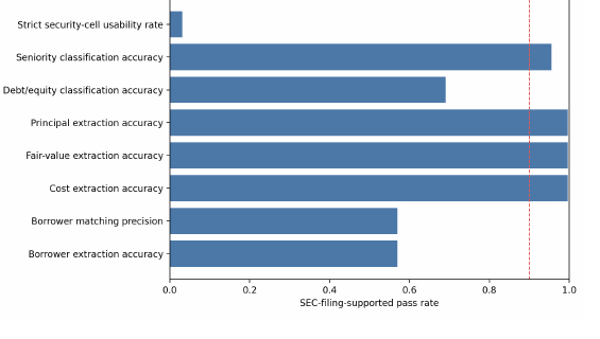

Public Windows into Private Credit: BDC Disclosures and Same-Borrower Valuation DisciplineDiogo Sampaio Lima2026Working paperPrivate credit has grown rapidly, yet outsiders rarely observe how individual private loans are valued. I use public filings by Business Development Companies (BDCs)—which hold private-credit-like loans and disclose position-level cost and fair value in their schedules of investments—to compare the values different BDCs report for the same borrower at the same reporting date. Reported marks differ across holders of the same borrower, and the differences are systematic. A BDC whose own portfolio is deteriorating marks a shared borrower lower than other holders do at the same date: in the pre-2026 homogeneous-debt sample, a 10 percentage point increase in the markdown on the rest of the portfolio predicts a 1.26 percentage point larger markdown on the shared borrower, identified from changes. The direction is the surprise. The bank fair-value literature finds that pressured institutions delay loss recognition to protect capital; pressured BDCs instead mark shared borrowers more conservatively. The relation concentrates in junior and structured debt, is absent in equally volatile first-lien positions, and carries no detectable power to forecast the borrower’s future deterioration, placing it in lender-side judgment rather than superior borrower information. Reported private-credit marks are thus not pure borrower signals: two lenders holding the same loan report systematically different values for reasons tied to the holder, not the borrower. A source-filing audit confirms that cost and fair-value extraction from public filings is highly reliable, so public BDC disclosures provide a scalable instrument for measuring private-credit valuation at the position level.

@unpublished{sampaiolima_private_credit, title = {Public Windows into Private Credit: BDC Disclosures and Same-Borrower Valuation Discipline}, author = {Sampaio Lima, Diogo}, year = {2026}, note = {Working paper}, } - WIPClimate and Sovereign Risk in Production EconomiesDiogo Sampaio Lima2026Work in progress

2025

- WP

Quantitative Easing and Sovereign Debt Maturity ChoiceDiogo Sampaio Lima2025Working paper

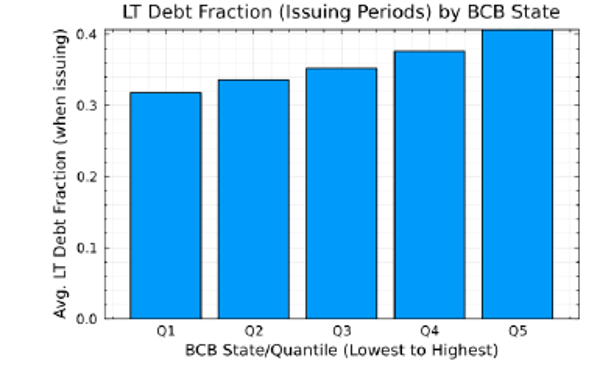

Quantitative Easing and Sovereign Debt Maturity ChoiceDiogo Sampaio Lima2025Working paperThe widespread use of unconventional monetary policies has fundamentally altered the environment for sovereign debt management. This paper investigates how sovereign governments should strategically manage their debt maturity structure when central banks are active participants in bond markets. Using Spanish data from 2009-2024, we provide empirical evidence that the Treasury systematically lengthens debt maturity in response to European Central Bank asset purchases. To rationalize this behavior, we develop a quantitative sovereign debt model with default risk where the government issues both short-term and long-term debt, and a central bank actively manages a bond portfolio. The key innovation is a portfolio balance channel where the term premium on long-term debt endogenously responds to the net supply of bonds held by private investors. The calibrated model successfully reproduces the empirical relationship: the long-term debt fraction rises as central bank holdings increase. Counterfactual analysis confirms that eliminating the variable term premium removes this systematic relationship entirely. Comparing a Strategic Treasury to a passive government constrained to fixed issuance mix reveals nuanced welfare trade-offs. The activist approach achieves consumption smoothing and benefits from strategic market timing, but exhibits higher default risk and lower sustainable debt levels.

@unpublished{sampaiolima_qe_maturity, title = {Quantitative Easing and Sovereign Debt Maturity Choice}, author = {Sampaio Lima, Diogo}, year = {2025}, note = {Working paper}, }

2023

- JFSGlobal Capital Flows and the Role of Macroprudential PolicyDiogo Sampaio Lima and Sudipto KarmakarJournal of Financial Stability, 2023

@article{sampaiolima_macropru_flows, title = {Global Capital Flows and the Role of Macroprudential Policy}, author = {Sampaio Lima, Diogo and Karmakar, Sudipto}, journal = {Journal of Financial Stability}, year = {2023} }